The Orthopedic Braces Market plays a vital role in supporting individuals with musculoskeletal conditions, offering a diverse range of orthopedic devices designed to provide stability, support, and pain relief. Among the myriad of orthopedic braces available, the orthopedic knee brace stands as a cornerstone of this market, offering targeted support for individuals with knee injuries or conditions such as osteoarthritis. These braces are meticulously designed to stabilize the knee joint, reduce strain on damaged ligaments, and alleviate discomfort during activities of daily living or sports participation. Within the Orthopedic Braces Market, orthopedic knee braces come in various styles and configurations, including hinged braces for added support and compression sleeves for mild to moderate knee injuries. By offering personalized solutions tailored to individual needs, orthopedic knee braces empower individuals to maintain mobility and pursue an active lifestyle despite orthopedic challenges.

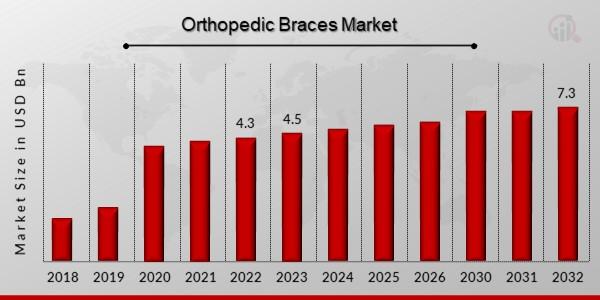

According to MRFR analysis, the Global size of the Orthopedic braces market was estimated at USD 4.3 billion in 2022. The worldwide demand for Orthopedic braces is anticipated to increase from USD 4.5 billion in 2023 to USD 7.3 billion by 2032, growing at a compound annual growth rate (CAGR) of 6.20% throughout the forecast period (2023-2032).

Regional Analysis

- Americas: Expected to lead the market, driven by increasing prevalence of osteoarthritis and rising per capita healthcare expenditure. Further segmented into North America (US and Canada) and Latin America.

- Europe: Divided into Western Europe (Germany, France, UK, Italy, Spain, and rest of Western Europe) and Eastern Europe. European market benefits from increasing geriatric population.

- Asia-Pacific: Anticipated to be the fastest-growing market, segmented into Japan, China, India, South Korea, Australia, and rest of Asia-Pacific. Rising geriatric population contributes to market growth.

- Middle East & Africa: Divided into the Middle East and Africa. Market growth influenced by increasing orthopedic procedures and healthcare infrastructure development.

Segmentation

- Product: Segmented into knee braces, foot and ankle braces, upper extremity braces, and others. Knee braces expected to be the fastest-growing segment due to their benefits in providing support and protection.

- Type: Segmented into soft and elastic braces, hinged braces, and hard braces. Soft and elastic braces anticipated to lead the market due to their ease of use and customization.

- Application: Segmented into ligament injury, preventive care, post-operative rehabilitation, osteoarthritis, and others. Ligament injury expected to hold the largest market share due to the increasing number of injuries globally.

- End User: Includes orthopedic clinics, hospitals, surgical centers, and others. Orthopedic clinics expected to dominate the market due to the growing number of orthopedic procedures performed in such facilities worldwide.

Addressing the prevalent issue of back pain, orthopedic belts emerge as essential devices within the Orthopedic Braces Market, providing targeted support and relief for individuals with lumbar spine disorders. These orthopedic belts, also known as back braces or lumbar supports, are designed to stabilize the lumbar spine, promote proper posture, and alleviate strain on the lower back muscles. Within the Orthopedic Braces Market, orthopedic belts for back pain are available in various designs, including elastic compression belts, rigid braces with adjustable support, and posture correction belts. Whether it's managing acute back injuries, supporting the spine during recovery from surgery, or preventing recurrent back pain, orthopedic belts offer a versatile and effective solution for individuals seeking relief from lumbar spine discomfort. By providing targeted support and promoting spinal alignment, orthopedic belts play a crucial role in enhancing comfort and functionality for individuals affected by back pain.

Key Players

Some of the key orthopedic braces companies are BSN medical (Germany), Bauerfeind (Germany), Breg, Inc. (US), Ottobock (Germany), DJO LLC (US), Weber Orthopedic Inc. (US), Frank Stubbs Company Inc. (USA), DeRoyal Industries, Inc. (US), THUASNE SA (France), and Aspen Medical Products (US).

For more information visit at MarketResearchFuture

Other Trending Reports