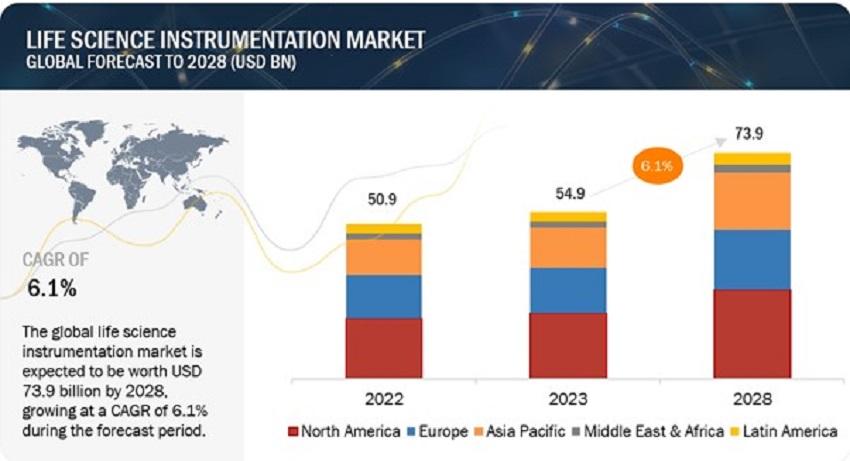

The global Life Science Instrumentation Market in terms of revenue was estimated to be worth $54.9 billion in 2023 and is poised to reach $73.9 billion by 2028, growing at a CAGR of 6.1% from 2023 to 2028. The increasing number of research grants, rising prevalence of chronic diseases, and rising focus on precision medicine are expected to drive the market during the forecast period.

Prominent players operating in the global life science instrumentation market are Thermo Fisher Scientific Inc. (US), Danaher Corporation (US), Agilent Technologies, Inc. (US), Waters Corporation (US), Shimadzu Corporation (Japan).

Download a FREE Sample PDF of the Global Life Science Instrumentation Market Research Report at https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=38&utm_source=Ganesh&utm_medium=P

This research report categorizes the life science instrumentation market to forecast revenue and analyze trends in each of the following submarkets:

By Technology

- Spectroscopy

- Chromatography

- Polymerase Chain Reaction

- Immunoassays

- Lyophilization

- Liquid Handling Systems

- Clinical Chemistry Analyzers

- Microscopy

- Flow Cytometry

- Next-Generation Sequencing (NGS)

- Centrifuges

- Electrophoresis

- Cell Counting

- Other Technologies

By Application

- Research Applications

- Clinical & Diagnostics Applications

- Other Applications

By End User

- Hospitals and Diagnostic Laboratories

- Pharmaceutical & Biotechnology Companies

- Academic & Research Institutes

- Agriculture & Food Industries

- Environmental Testing Laboratories

- Clinical Research Organizations

- Other End Users

By technology, the spectroscopy segment accounted for the largest share of the life science instrumentation market in 2022.

Based on technology, the global market is segmented into spectroscopy, chromatography, PCR, immunoassays, lyophilization, liquid handling, clinical chemistry analyzers, microscopy, flow cytometry, NGS, centrifuges, electrophoresis, cell counting, and other technologies. In 2022, the spectroscopy segment accounted for the largest market share. The rising use of advanced instruments in oncology research and the need for better sensitivity and enhanced speed is driving the segment growth.

By end user, the pharmaceutical & biotechnology companies segment accounted for the largest share of the life science instrumentation market in 2022.

Based on end user, the global market is segmented into hospitals and diagnostic laboratories, pharmaceutical & biotechnology companies, academic & research institutes, agriculture & food industries, environmental testing laboratories, clinical research organizations, and other end users. In 2022, pharmaceutical & biotechnology companies accounted for the largest market share. The highest share of this segment is attributed to significant use of life science equipment for the development of medication and rise in R&D.

Direct Purchase of the Global Life Science Instrumentation Market Research Report at https://www.marketsandmarkets.com/Purchase/purchase_reportNew.asp?id=38&utm_source=Ganesh&utm_medium=P

By application, the research applications segment of the life science instrumentation market to register significant growth in the near future.

Based on application, the global market is segmented into research applications, clinical & diagnostic applications, and other applications. Research applications to register the highest growth rate during the forecast period. The major factors responsible for the highest growth rate of this segment are the availability of funding for R&D in academic institutes.

By region, North America is expected to be the largest region in the life science instrumentation market during the forecast period.

North America, comprising the US and Canada, accounted for the largest market share in 2022. Factors such as growing funding for research, and increasing applications in the healthcare/medical sector, and presence of major players in the region are driving market growth in North America.